This month: Washington invents a new tax without calling it a tax: a 15% skim on chip sales to China in exchange for export licenses. Inside the enterprise, AI adoption is widening divides by gender and seniority—governance can close it. And in boardrooms, independent directors are acting more like hands‑on advisors than ceremonial overseers.

The 15% Toll Booth

President Trump cut an unprecedented deal: Nvidia and AMD can sell certain AI chips into China if they hand 15% of revenue from those sales to the U.S. government. Commerce has begun issuing licenses for Nvidia’s H20; the White House has even floated a degraded version of Blackwell next. This isn’t industrial policy; it’s a cover charge.

If a chip posed a national‑security risk in April, it doesn’t become “safe” in August because Uncle Sam gets a taste. It’s been reported that Trump said he wanted 20% and “negotiated” down to 15%, and that the deal covers Nvidia’s H20 and a slowed AMD “MI308.” China, meanwhile, is discouraging the use of H20 in sensitive settings. Markets like clarity; this is improv.

Investors will tell themselves it’s manageable. Bernstein analysts estimate the fee cuts gross margins on China‑bound GPUs by 5–15 points, shaving roughly 1 point off overall margins—material but not thesis‑breaking for Nvidia. That’s the point: the fee is small enough to normalize, big enough to normalize pay‑to‑play.

Why it matters:

Rule of men, not rules of law. Pricing export controls like a nightclub wristband blurs the line between security and dealmaking, inviting copycats in other “strategic” sectors.

Model risk explodes. Investors are no longer modeling tariffs or bans—they’re modeling presidential discretion by quarter.

Geopolitical whiplash. Beijing is nudging buyers away from H20, muting volumes and dulling Washington’s leverage. Expect demand substitution and more “China‑only” SKUs to game the next line in the sand.

Precedent isn’t made in rule books — it’s made in back rooms. Once a president monetizes a security restriction, every sector in Washington’s sights has to wonder what its “price” will be. Investors should expect more one-off bargains and fewer clean policy lines. Operators should build agility into plans—not just for market swings, but for rule-of-law whiplash. And citizens? We should be clear-eyed. A toll booth on capitalism might collect from the right travelers today, but it won’t stay in one lane forever.

Close the AI Gap Before It Widens Workplace Inequality

Inside most companies, AI isn’t a great leveler—it’s a wedge. Multiple surveys show men use gen‑AI more than women (Deloitte: 44% men vs. 33% women in 2024; BIS: 50% vs. 37% in a U.S. sample). Women are also more wary of AI’s impact, which depresses uptake. Meanwhile, frontline adoption has hit a “silicon ceiling” around 50%, while leadership teams race ahead. Left alone, this becomes BYO‑AI—shadow tools, uneven productivity, and inequity.

The fix isn’t a memo. It’s governance + enablement:

Clear, permissive guardrails. Define approved use cases and banned ones (PII, MNPI). Require human‑in‑the‑loop sign‑off for legal, regulatory, and investor‑facing outputs. (IR teams should treat AI output like an intern’s first draft.)

Access + role‑based training. Two‑thirds of leaders won’t hire without AI skills, yet only ~39% of users have received employer training. Close that gap with short, role‑specific sessions tied to actual workflows.

Prompts, not platitudes. Publish a prompt library by function (IR, Legal, Comms, Sales) and keep it in version control.

Attribution & logs. Add internal footers for AI‑assisted docs; disclose externally when material. Keep change logs for anything touching filings, earnings, or clients. (Yes, most people also want AI to credit sources—align with that norm.)

A real committee. Stand up an AI policy committee (IR, Legal, IT/Sec, Comms, HR) with the authority to approve tools, sandbox agents, and measure ROI. If you want a practical template that works in the real world, let’s talk—I can walk you through one.

Companies that ship inclusive AI rules (access + training + attribution + sign‑off) will hit gender parity in adoption and show measurable gains in workforce satisfaction and output in a single quarter. Those that don’t will watch usage gaps calcify into promotion gaps. The choice isn’t whether employees use AI—it’s whether they’ll do it in daylight with trust, or in the shadows with risk.

From the Field Next-Gen Boards Want Hands-On Advisors

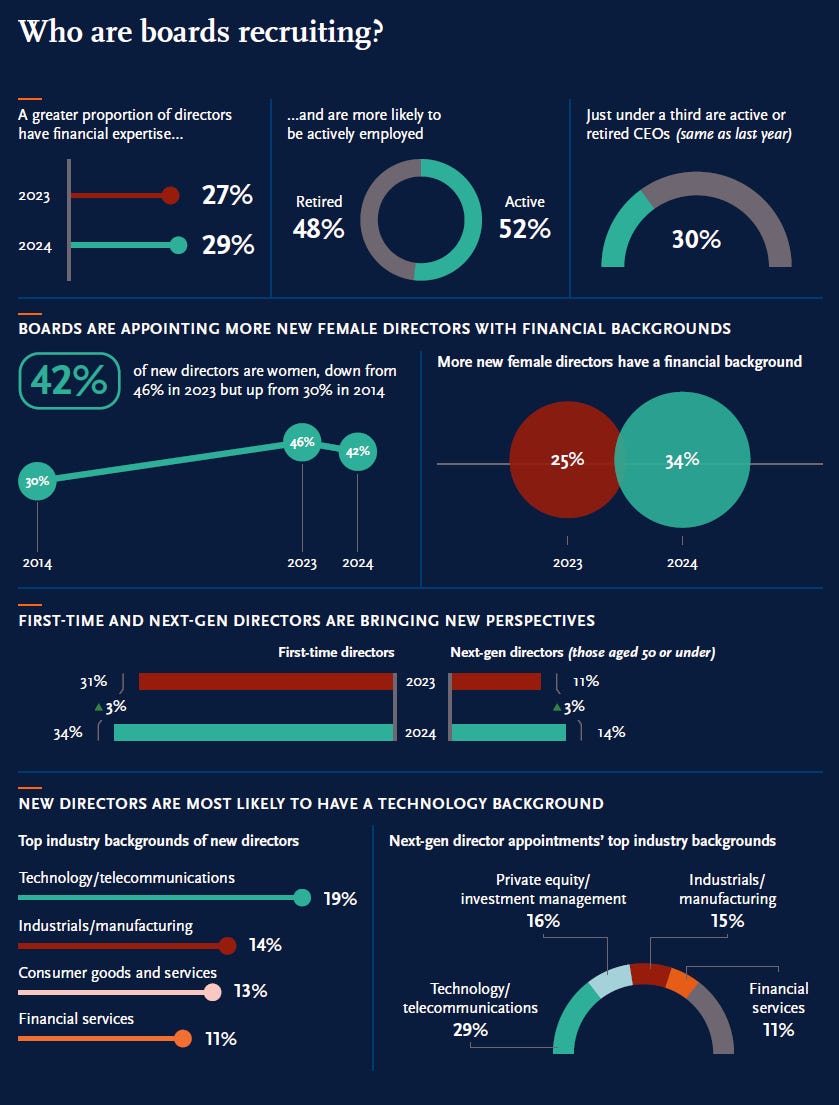

Boards are moving from periodic oversight to active advising — and the talent profile is changing with it. Nominating chairs say refreshing for new skills is the top priority. “Next‑gen” directors (age 50 or under) made up 14% of 2024 appointments, up from 11% the prior year; 89% of that cohort are actively employed, and 29% come from tech/telecom. First‑time directors account for 34% of new seats. Translation: boards are recruiting hands‑on operators who can stress‑test strategy and communicate it to markets and stakeholders — including capital markets, IR, comms, and digital fluency.

Source: SpencerStuart

The architecture is catching up. Standalone science and technology committees appear on 17% of S&P 500 boards, up from 10% in 2019, and core committees now meet roughly 8.1 (Audit), 5.7 (Comp), and 4.6 (Nominating) times a year. That’s a clear signal: more scope and more work for directors with domain depth who can pressure‑test plans without crossing into execution. The best boards set crisp advisory lanes and keep a light record of between‑meeting touchpoints so engagement stays high and independence stays intact.

Signal vs. Noise

The 15% Precedent — When national security gets a cover charge, investors aren’t pricing chips—they’re pricing presidential whim disguised as policy.

AI Parity Needs Rules — Without access, prompts, and attribution, AI lifts insiders and sidelines juniors; governance is inclusion, not bureaucracy.

Boards, Not Bystanders — Independent directors are stepping up as active advisors; the winners will set clear lanes that sharpen accountability.

One Last Thing — License On, License Off

I don’t think this deal will hold steady — the terms, fees, and chip lists will change again and again. Ten revisions wouldn’t surprise me. Commerce is already licensing the H20, the White House is floating a cut-down Blackwell, and Beijing is nudging buyers elsewhere. Investors should start pricing in policy churn as part of the thesis. Business leaders should treat constant rule changes as the baseline, not the exception. In this market, agility isn’t a hedge. It’s survival.

If this letter resonated with you—or you just want to keep our conversation going—I’d love to hear from you.

Until next month,

— Zachary