This month: We look at how value — and risk — increasingly accumulate off the balance sheet, why accountability breaks when decision rights are unclear, and how conviction becomes dangerous when it stops updating. In markets that reward speed and certainty, the real edge still belongs to those who can see what’s quietly compounding — and pause long enough to think clearly about it.

Intangible Liabilities

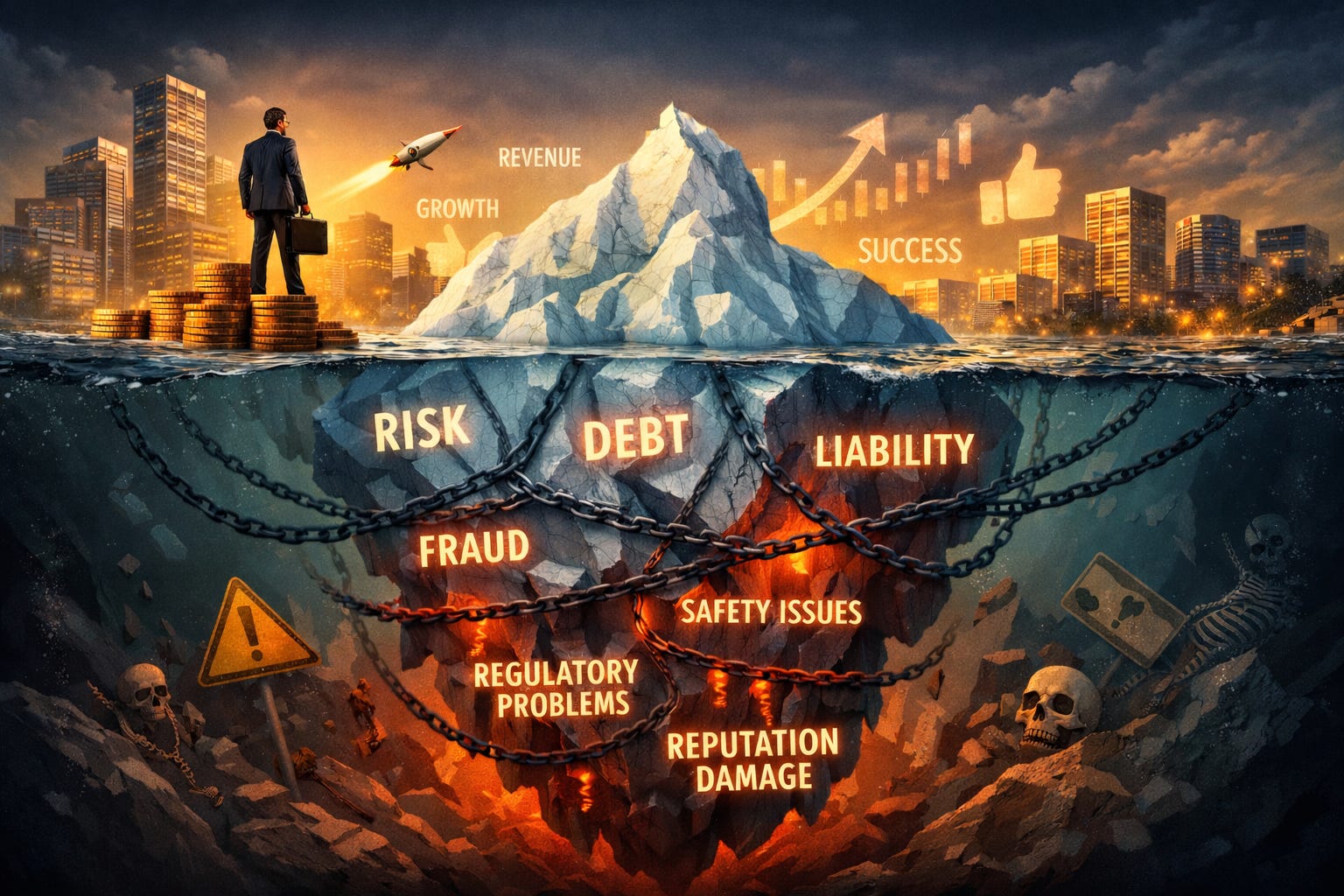

If you’ve been reading my newsletter for a while, you know I spend a lot of time thinking about intangible assets — the things companies pay for every day that never quite make it onto the balance sheet. Brand equity. Trust. Design. Distribution. Culture. These are real economic assets. They’re funded through operating expenses, run through the income statement, and never capitalized under GAAP. The value compounds quietly and shows up indirectly in pricing power, resilience, or a higher multiple.

Lately, I’ve been thinking about the mirror image of that idea.

If a company can spend money over time building intangible assets that accounting doesn’t recognize, can the opposite also be true? Can a company be generating revenue on the income statement while steadily compounding an off-balance-sheet liability?

In other words, can you be earning money today in a way that is systematically building a future obligation — one that won’t show up as a liability until it arrives all at once?

Consider a familiar example. A company ships a product faster than it’s ready. Customers buy it. Revenue is booked. Cash comes in. On paper, things look healthy. But behind the scenes, shortcuts are being taken in quality, controls, data discipline, safety, or disclosure. None of that shows up as a balance-sheet liability. Not yet. What does show up are the benefits: growth, momentum, maybe even praise for execution speed.

The liability is real, but it’s not recognized because it isn’t yet “probable” or “measurable.” It’s invisible until it isn’t.

This isn’t just about any one technology or trend. It’s a broader pattern. Companies routinely earn money in ways that accrue reputational debt, regulatory debt, security exposure, quality risk, or credibility erosion, liabilities that aren’t booked as obligations. The income statement captures the upside. The balance sheet stays clean. Right up until the moment it doesn’t.

Yes, companies disclose risk factors. But those are qualitative warnings, not economic recognition. They tell you what could go wrong, not what is actively accumulating as a result of day-to-day operating choices.

The uncomfortable truth is that modern companies are very good at measuring what they earn, and much worse at measuring what they owe in the future — especially when that obligation is being built gradually, invisibly, and profitably.

Intangible assets compound quietly. So do intangible liabilities.

And markets have a long history of repricing companies, not when those liabilities are created, but when they finally become undeniable.

My Three A’s

I talk about these ideas a lot in my work. They’re deceptively simple, and yet so many organizations get them wrong.

Autonomy. Authority. Accountability.

For me, these are the foundations of good leadership and effective management. And I often come back to the same question: if you’re not going to give your team autonomy to work independently, authority over their domain, and accountability for their outcomes, why do you even have a team?

Most companies say they want ownership. What they actually design is something else.

The most common failure mode is accountability without authority. Teams are expected to “own” results, but key decisions live elsewhere. Approvals stack up. Dependencies multiply. When outcomes disappoint, shit rolls downhill. Accountability becomes a risk, not a privilege.

The inverse, authority without accountability, is just as corrosive. Decisions get made freely, but consequences never land. Over time, this breeds empire building and internal politics. Power accumulates; learning does not.

Then there’s autonomy without accountability, which sounds empowering but usually produces drift. Freedom without ownership isn’t empowerment — it’s abdication.

And perhaps the most corrosive is autonomy without authority. The gnawing frustration of being told you’re empowered, right up until the moment you actually try to decide something.

None of this is philosophical. It’s mechanical.

A simple diagnostic I use with executives: who can say yes, who can say no, and who pays the price if it’s wrong?

If you can’t answer those three questions clearly, you don’t have autonomy, authority, and accountability. You just say you do.

There’s also a language problem embedded here. Many teams use “accountable” and “responsible” interchangeably. They’re not the same. Responsibility is about tasks. Accountability is about outcomes. One lives in project plans. The other lives in incentives, reporting lines, and how leaders behave when results miss.

When these three A’s are aligned, something powerful happens. Speed increases without chaos. Decisions move closer to the information. Leaders stop being bottlenecks. And accountability becomes motivating instead of punitive.

When they’re misaligned, organizations compensate with process, meetings, and oversight. That works for a while. Eventually, it just slows everything down.

Autonomy, authority, and accountability aren’t soft leadership concepts. They’re design constraints. Get them right, and execution scales. Get them wrong, and no amount of vision or culture work will save you.

From the Field: Stubbornness vs. Conviction

One of the hardest things in markets is telling the difference between conviction and stubbornness, since both feel like courage in real time.

Both involve holding a position while the market disagrees with you. Both get justified as long-term thinking. And both are rewarded, briefly, often enough to reinforce the behavior.

The difference only becomes clear later.

Conviction is the ability to hold through volatility while remaining open to updating your thesis as facts change. Stubbornness is holding with the same confidence, but gradually losing the ability to see new information clearly.

This distinction shows up in process, not posture. Investors with conviction tend to have already thought through what would make them wrong. They have a view on which indicators matter early and which lag. They know the difference between noise in the price and signal in the fundamentals.

Stubbornness, by contrast, narrows the aperture. New information is filtered to protect the original story. Misses are framed as temporary. Structural shifts are dismissed as cyclical. The thesis stops being tested and starts being defended.

Markets make this especially treacherous because they often reward both behaviors — at least for a while. A stock can bounce without the business improving. Narrative can outlast reality. That’s how broken strategies get doubled down on, and how good ones get abandoned too early, with “pragmatism” disguising weak hands.

What the last few years have made clear is that the premium doesn’t belong to the loudest conviction or the fastest reflexes. It belongs to investors who can hold through volatility and update quickly when facts change.

That combination is rarer than IQ. And markets pay for it.

Signal vs. Noise

Off-Balance-Sheet Risk — Markets don’t punish risk-taking; they punish surprise. The most dangerous liabilities aren’t disclosed in footnotes or priced into models. They’re the ones quietly compounding while earnings still look clean.

Decision Rights Tell the Story — Culture isn’t revealed by what’s written down. It shows up in who decides when it matters. Authority appears in moments of stress. Accountability arrives after the fact.

Courage Has a Process — Conviction without update rules is just stubbornness with better branding. The real edge belongs to investors and leaders who can hold through volatility and revise when facts change.

One Last Thing

Value rarely disappears overnight. It’s usually preceded by a long period where decisions feel justified, results look fine, and important signals stay just out of view. The real edge — for companies and investors alike — comes from noticing what’s invisibly compounding and having the discipline to adjust before the math makes the decision for you.

If this letter resonated, I’d love to hear from you.

Until next month,

— Zachary