This month: This month: U.S. Treasuries behave less like a refuge and more like a risk asset, raising questions that used to be unthinkable. AI capex brings old capital-cycle math back into view, with tangible assets reshaping outcomes faster than stories can. And in a year defined by speed, we look at why the best ideas still come from slowing down.

Is the U.S. an Emerging Market?

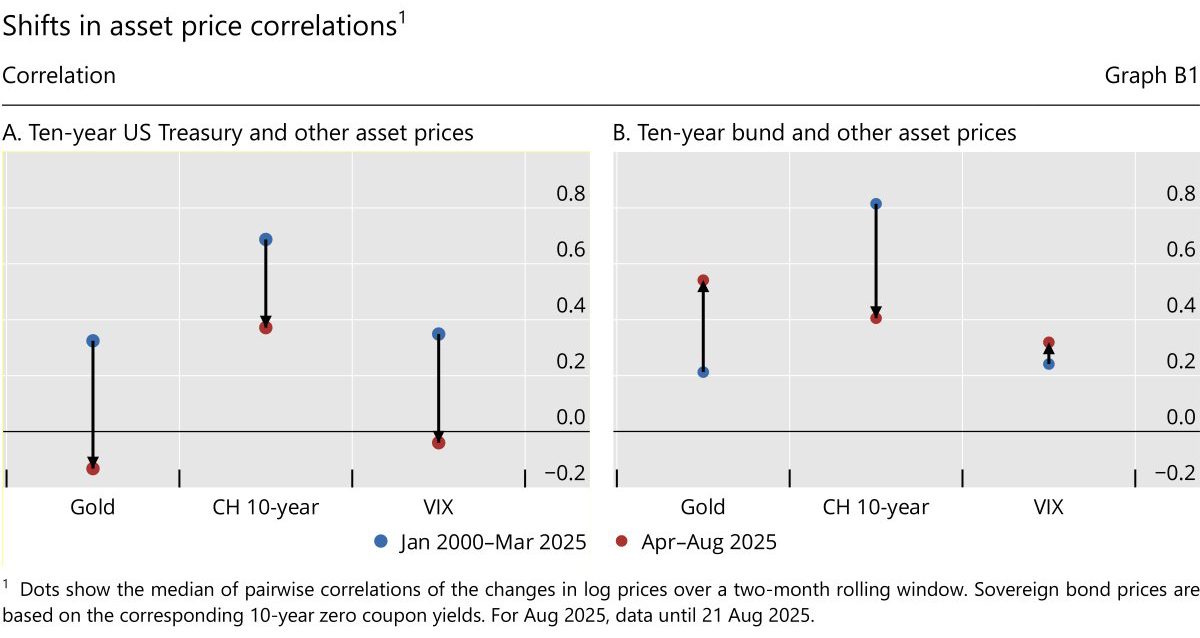

If you want to know whether a country is “developed” or “emerging,” don’t look at the flag. Look at what its government bonds do on bad days.

In a classic developed‑market panic, equities sell off, the VIX spikes, and government bonds rally as investors sprint for safety. In 2025, that script started to break. Around the April tariff shock, equity volatility jumped and risk assets sold off — but long‑dated treasuries also sold off, sending yields higher instead of lower.

That was not a one-off quirk. Research from the BIS and others shows that the old safe-haven pattern, where treasuries tended to move opposite to risk assets, has weakened. Correlations that were predictably negative for decades have moved toward zero. In several 2025 stress periods, treasuries did not provide their usual offset to equity volatility. What had long been a stabilizing relationship instead became another source of uncertainty.

Source: BIS Quarterly Review, September 2025

The preconditions that made bonds a dependable hedge, including low and stable inflation, unquestioned policy credibility, and modest public debt, are rarer. Studies on safe assets point to creeping fiscal dominance. Markets increasingly assume central banks are constrained by the need to finance large and growing deficits rather than focus solely on inflation. It is telling that big allocators like BlackRock have tilted away from long treasuries, citing structurally higher issuance and funding needs.

This is how emerging markets trade. Local government bonds are not “risk-free”; they are credit, a rolling vote on fiscal math, politics, and the capacity of the central bank to say “no” to the government. By that standard, the U.S. increasingly looks like the world’s most sophisticated emerging market, still the benchmark but now carrying a risk premium that shows up not just in yield but in behavior when the herd is scared.

If that regime holds, the knock-on effects are straightforward and uncomfortable. Anything priced off the “risk-free rate” inherits more policy and refinancing risk. Balance sheet quality, including terming out debt, maintaining liquidity, and managing reliance on short-term funding, starts to matter as much to equity multiples as the growth story. Stress events become less about earnings misses and more about who can roll their obligations on days when treasuries themselves are selling off.

In other words, the U.S. may not be an emerging market, but its bonds have been trading like it is.

Daydream More

Some of my best work happens when I look like I’m doing nothing. The instinct is always to be in motion — reading, modeling, on calls — but the real shifts usually show up in the gaps, not the grind.

Away from markets, the clearest example coming to mind as I write this is my garage woodshop. When I was first setting up my shop, I spent an embarrassing amount of time just standing in an empty room. Not measuring or sketching, just staring at the walls with a beer in my hand, imagining what might live where. I’d walk away, come back the next day, stare some more. Slowly, the space started to make suggestions: the light wants the bench here; dust collection has to go there. Only after a lot of supposedly “wasted” time did an actual plan come into focus.

Investing is weirdly similar. Screens make it feel like the job is to ingest quotes, feeds, filings, and research constantly. But the inflection points do not usually arrive in the fifteenth PDF. They show up on a walk, in the shower, or in a moment when your mind has room to quietly rearrange what you already know into a different pattern.

With all the focus on AI these days, it struck me that this is one thing AI cannot do for you. Models are extraordinary once you give them a defined task: summarize this, rewrite that, generate ten scenarios. What they do not have is that garage moment, with no blank space, no open-ended “what if,” and no spidey sense that something about a company or a cycle does not quite add up.

For investors, founders, and anyone making directional bets, the scarce resource isn’t information anymore. It’s unused attention. If every idle minute is filled with another podcast or scroll, there’s no oxygen left for the slow, slightly uncomfortable experience of thinking for yourself.

I’ve started to treat those blank, unproductive hours — in the garage, between meetings, staring out a window — as part of the job, not a break from it. The market will never see that time on a slide, but most of the “obvious in hindsight” calls come from there.

From the Field: Capital-Light, Capital-Heavy

The surge in AI-related capex has become a kind of Rorschach test. Some executives see the need for reinvestment, while others see a replay of old capital cycles. It has also brought some of the sharpest thinkers on intangibles back to the world of physical assets, including Kai Wu of Sparkline. Kai is well known for his work on intangible value. In his latest research, he flips the lens to tangible balance sheets.

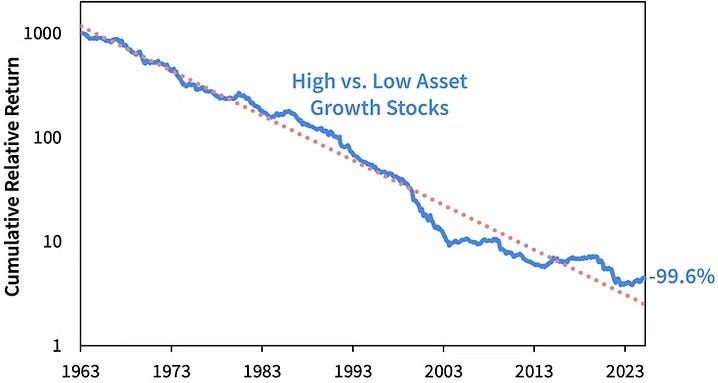

His study of the “asset-growth anomaly” reveals a consistent and measurable pattern. Companies that rapidly add physical assets such as servers, real estate, logistics networks, or manufacturing capacity have underperformed their more asset-light peers by roughly 8.4 percent a year. This holds true across sectors and time. The AI spending boom is simply the newest version of that dynamic.

The chart below shows how consistently high asset growth has lagged more disciplined balance-sheet strategies over time.

Source: Surviving the AI Capex Boom

Wu’s point is not that capex is bad. It is that heavy assets reshape a business faster than most leaders expect. They depreciate, require upkeep, and slow return cycles, and ultimately, optionality narrows as the balance sheet gets heavier. The payoff can be real, because many moats are built on concrete rather than code, but the burden grows just as fast.

I am seeing the same tensions in my client work. Some companies are scaling AI infrastructure. Others are expanding logistics networks or buying real estate to gain more control over their operations. These are different plays, yet they raise the same question for the investor in me. Do these assets improve the business's return profile, or do they just add weight?

Asset-light firms tend to show more resilience. They reinvest faster. They carry less operating leverage. Their models scale without adding steel or land. This does not mean asset-heavy strategies are misguided. It means the market is getting better at distinguishing between assets that create advantage and those that absorb capital.

AI may be the headline, but the deeper theme is broader. In an economy where flexibility has become a real moat, the weight of the balance sheet is harder to ignore.

Signal vs. Noise

Safe Havens, Rethought — When government bonds stop behaving like ballast, everything priced off them inherits the uncertainty. That is not volatility. That is architecture shifting.

The Cost of Concrete — AI spending grabs headlines, but the deeper signal is structural. Capital-heavy balance sheets don’t just slow returns. They harden a company’s future into a narrower set of outcomes.

The Quiet Advantage — In a world where information is instant and infinite, the scarcest asset is uninterrupted thought. Leaders who protect that space will see around corners that others scroll past.

One Last Thing

In a cycle obsessed with speed — faster chips, faster data, faster takes — the real advantage may come from the few willing to slow down. Markets eventually reward clarity over momentum, and clarity rarely arrives on a deadline.

If this letter resonated with you—or you want to keep this conversation going—I’d love to hear from you.

Until next month,

— Zachary