This month: Buffett’s timely wisdom on tariffs, how global rotation might signal a return to value, and rediscovering investing basics from my son’s notebook.

Buffett on Tariffs: A Master Class in Nuance (and Timing)

All eyes are on Omaha this weekend as Warren Buffett steps onto the stage for Berkshire Hathaway’s Annual General Meeting. Investors always anticipate insights on markets, valuation, and strategy—but this year, they’ll be especially attuned to Buffett’s perspective on tariffs and trade.

Why the heightened anticipation?

Two decades ago, in a famous 2003 Fortune article, Buffett sounded a dramatic alarm about America’s persistent trade deficits, likening the U.S. to an affluent family financing its lifestyle by slowly mortgaging the family farm to foreign creditors. His vivid parable of two fictional islands—Thriftville, the disciplined exporter, and Squanderville, the reckless debtor—highlighted a stark warning: chronic trade imbalances gradually transfer national wealth overseas, jeopardizing future generations’ prosperity.

Yet Buffett has always maintained skepticism about the wisdom of indiscriminate tariffs. In 2018, amid rising U.S.-China tensions, he reassured investors that tariffs, while disruptive and inflationary, were unlikely to devolve into a full-blown trade war because neither country would act “extremely foolishly” against its own self-interest.

Fast-forward to last month: new, sweeping tariffs from the Trump administration triggered global market turmoil. Misleading social media claims suggested Buffett supported these tariffs—prompting Buffett’s team to issue a rare public denial, clarifying he had made no remarks and would remain silent on the subject until Berkshire’s annual meeting.

That moment arrives this weekend.

Given Buffett’s longstanding nuanced position—deep concern about persistent trade deficits combined with skepticism about blunt tariffs—his upcoming comments will be essential listening. Buffett understands tariffs often act as hidden taxes on consumers, create inflation, and invite unintended retaliation. Yet, he’s equally clear that ignoring trade deficits indefinitely could have devastating long-term effects.

I, for one, can’t wait to hear his insights. Buffett excels at cutting through market noise, highlighting crucial nuances in complex debates. As markets await direction, his voice will carry significant weight—not just for investors, but for anyone making sense of how trade shapes our economic future.

The Real Rotation: All About Style, Not Geography?

Markets have been buzzing about a rotation out of U.S. stocks into international markets—particularly Japan and emerging economies. Recent flows back that up: capital is moving abroad, and at first glance, it looks like investors are chasing geographic diversification.

But that might not be the full story.

Yes, money is leaving U.S. equities. But what many of these international markets share isn’t geography—it’s valuation. Consider current P/E ratios:

S&P 500: 27.94

MSCI Emerging Markets: 15.29

MSCI Japan: 16.17

MSCI Brazil: 11.05

That’s not just a regional gap—it’s a style signal.

What we could be seeing is less a rotation out of the U.S., and more a rotation out of expensive stocks. Investors may not be repositioning by country—they may be repositioning by valuation. And if capital is flowing toward value internationally, it may not be long before that appetite returns to overlooked value names within the U.S. as well.

Here’s the insight: what looks like global rebalancing could be signalling something bigger. A long-overdue style shift—from growth to value—might be underway.

The Watchlist Mindset

Lessons from a 10-Year-Old

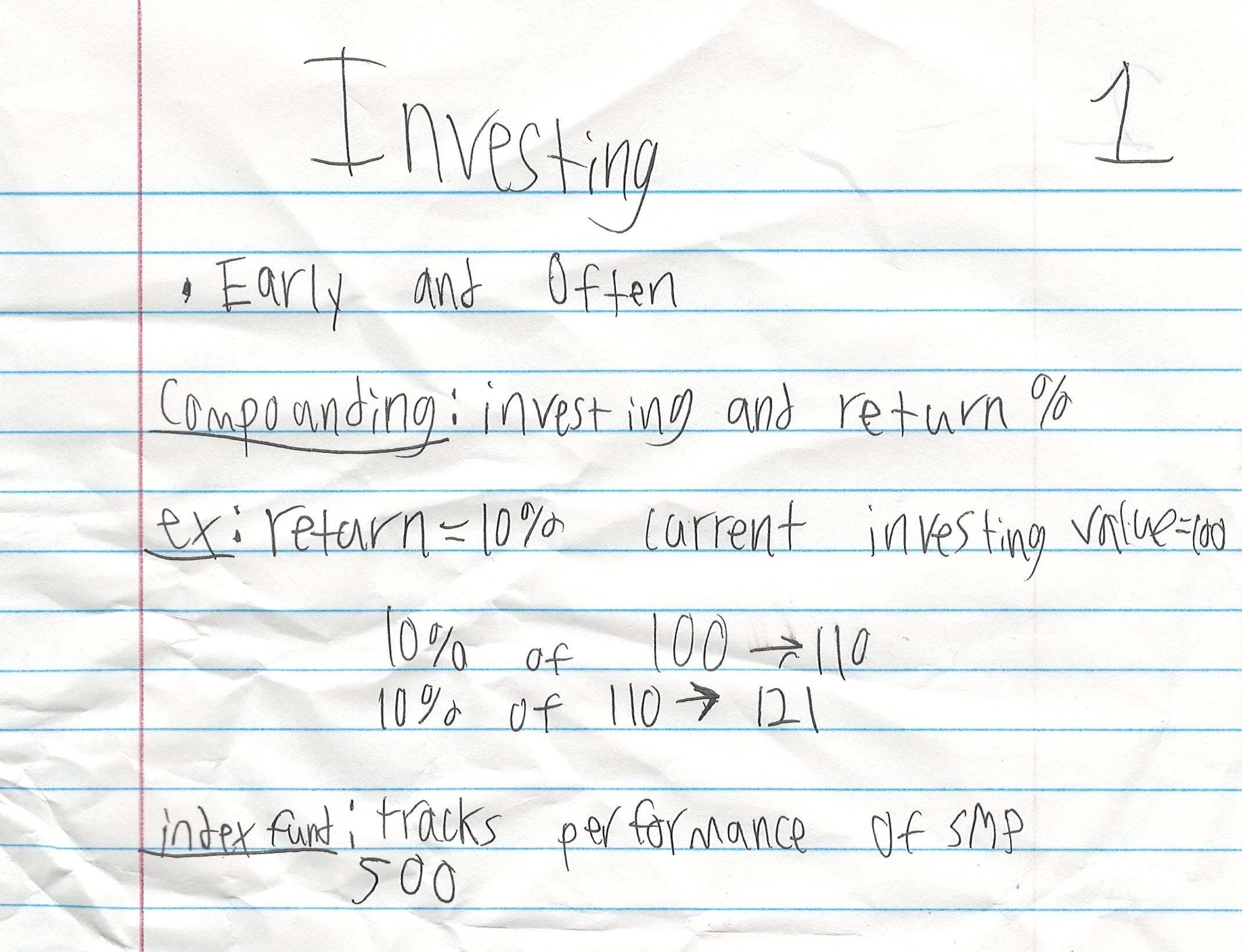

The other night, I picked up a crumpled notebook page from the floor of my 10-year-old son’s room. Expecting some sketches or perhaps a random scribble, I found something far more meaningful—notes he’d taken on investing:

Investing

Early and Often

Compounding: investing and return %

Ex: return = 10%, crrent investing value = 100

10% of 100 → 110

10% of 110 → 121

I stood there smiling—partly out of surprise, partly from pride—but mostly because I recognized something familiar. These were concepts I’d discussed often, sure, but here was my son, barely into double digits, genuinely exploring these ideas without being asked. It was the kind of moment every parent quietly hopes for: evidence that your words haven’t just bounced off, but sunk in deeply enough to spark genuine curiosity.

His notes weren’t fancy or filled with financial jargon. But that’s precisely what made them so compelling. They captured perfectly a core truth that even experienced investors sometimes overlook: compounding isn’t glamorous—it’s slow, steady, and remarkably powerful.

In a world where market noise pulls investors toward the quick wins and shiny trends, my son’s quiet exploration was a refreshing reminder. Real success in investing isn’t about timing markets perfectly—it’s about understanding a few good principles deeply and letting them quietly do their work over time.

As someone once said to me, “the two most important lessons in life are compound interest and Robert’s Rules of Order.” Seeing my son’s notes reminded me that understanding compounding might indeed be one of the most important lessons he’ll ever learn.

Signal vs. Noise

Buffett’s Real Message: Beware simplistic solutions like broad tariffs, but also recognize the serious long-term danger posed by persistent trade deficits. Balance matters, nuance matters—Buffett’s insights this weekend will be essential listening.

Global Rotation Could be Style, not Geography: Capital flowing internationally may signal a deeper shift toward value investing, one that might soon play out domestically. Revisit your own U.S. value watchlist accordingly.

Investing Fundamentals Still Win: In turbulent times, clarity comes from basic principles: consistency, patience, and the long-term discipline of compounding.

One Last Thing

Most economists agree that tariffs are inflationary. But that only holds if people keep buying the goods that have been taxed.

A 2% tariff on everyday items? Prices go up, people grumble, and inflation ticks higher. But a 145% tariff? That’s not inflation—that’s demand destruction.

Buffett warned years ago that tariffs are just taxes in disguise. But can something really be taxed if no one’s willing to buy it?

If this letter resonated with you—or you just want to keep our conversation going—I’d love to hear from you.

Until next month,

— Zachary