This month: AI moves from pilots to rewired workflows, with CEOs and boards pulled into ownership. Director sentiment rises slightly but stays cautious, shaped more by politics than fundamentals. And under the index’s calm surface, dispersion reminds us that volatility is the rule, not the exception.

AI, From Demos to P&L (and the CEO Owns It)

After two years of pilots, the question has shifted from “Can we demo it?” to “Did workflows change?” McKinsey’s latest survey finds more than three‑quarters of organizations now use AI in at least one function. Among these, 28% say the CEO oversees AI governance, 17% cite the board, and on average, two leaders share the responsibility. And 21% report they’ve fundamentally redesigned at least some workflows.

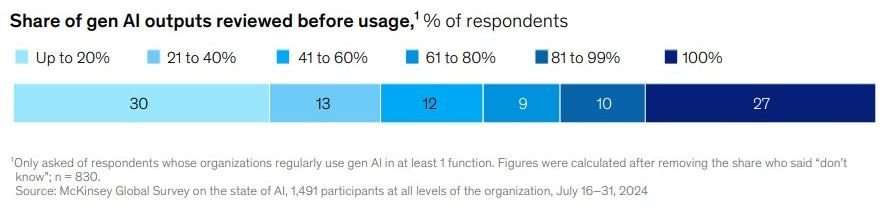

Oversight and controls are maturing unevenly. About 27% of organizations review all gen-AI outputs before use, while a similar share review 20% or less. Risk and data governance are usually centralized, while tech talent and adoption are more hybrid—a split that helps explain uneven quality control.

Source: McKinsey Global Survey

It’s still early days. In a companion survey, only 1% of executives describe their gen-AI rollout as “mature.” Less than one‑third say they’re following most adoption/scaling practices, and tracking well‑defined KPIs is the practice most correlated with bottom‑line impact—yet fewer than one in five say they track such KPIs today. Meanwhile, organizations report stepping up mitigation of inaccuracy, IP, and privacy risks, with nearly half having experienced at least one negative consequence from the use of gen-AI.

What to watch this quarter:

A clear accountability line for AI (including CEO/board oversight).

Evidence of workflow redesign (cycle‑time cuts, error rates, sales‑per‑rep).

Documented review thresholds for gen‑AI outputs and how they evolve.

A concise risk‑controls slide (IP, accuracy, privacy) rooted in actual processes.

Boardroom Weather Report

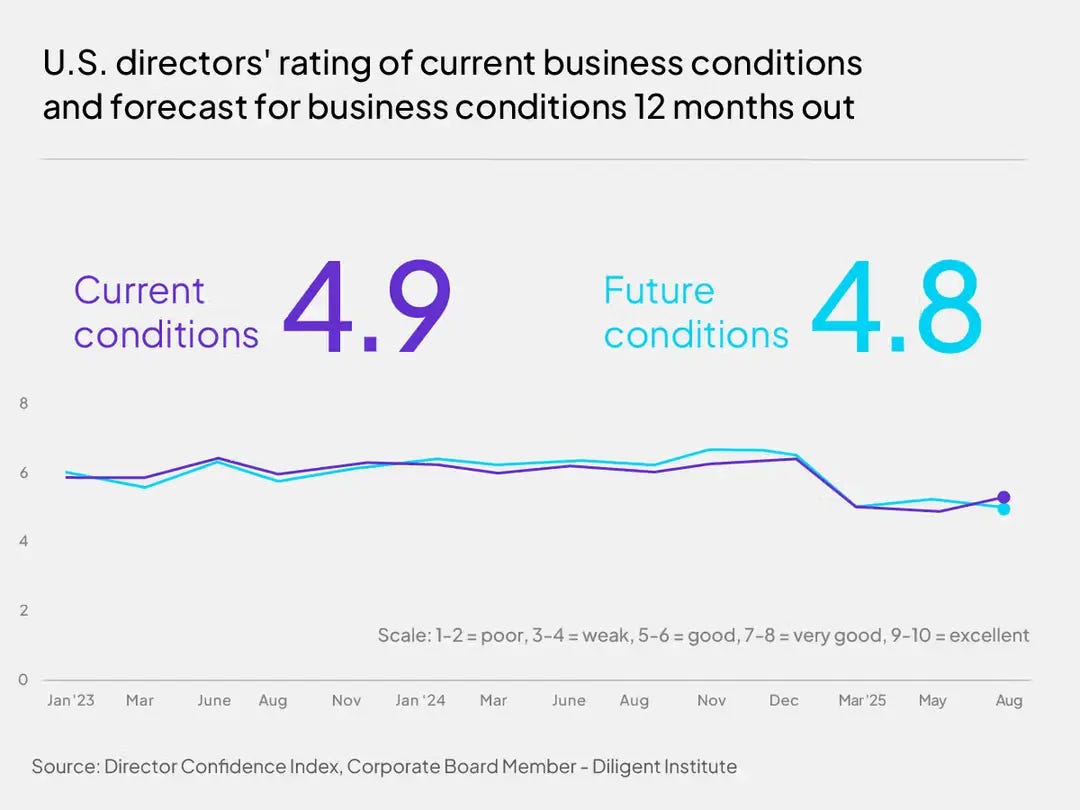

Directors read the landscape as mixed but manageable. The August Director Confidence Index shows current conditions at 4.9/10 (up from 4.4 in Q2) and a 12‑month outlook at 4.8/10. Policy is the main headwind in commentary. AI is the most‑cited opportunity. It’s a stance of preparation rather than pessimism.

Source: Diligent Director Confidence Index

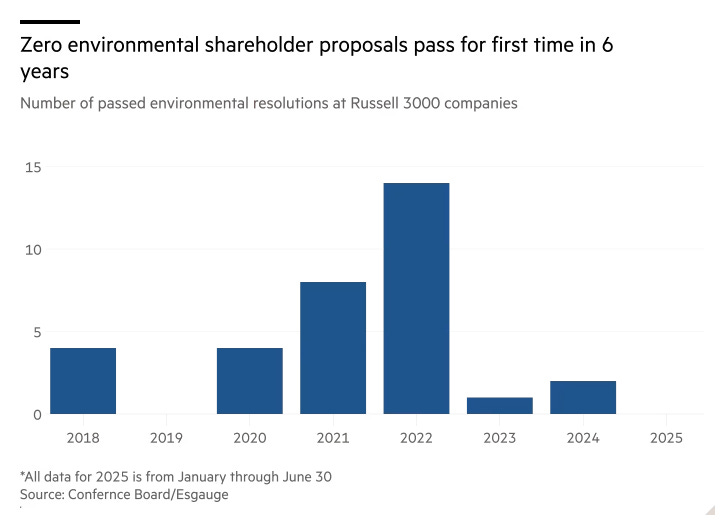

Proxy voting tells a similar story. In the 2025 proxy season, no U.S. environmental proposals cleared 50% support, while most majority wins clustered in governance topics. Independent reviews confirm the same shift: weaker backing for E-proposals and a return to core performance and rights.

Source: Financial Times

The near-term implication is straightforward: guidance and engagement tend to focus on what can be observed and tested. Boards are adding scenarios, tracking how policy transmits to demand and capex, and emphasizing metrics that can withstand a noisy tape. Expect ranges over declarations and a premium on operating proof. The watchword is calibration, not caution.

From the Field Living with Dispersion

I often return to the concepts of the Novel Investor’s post “Stocks Can Fluctuate Widely in a Year.” The numbers are dated, but the idea holds. In that sample, the S&P 500’s 52-week range was ~26%, while the average stock’s was ~56% (median ~46%); only 50 names had a narrower range than the index. It’s a reminder that indices smooth what individual stocks actually go through.

This year echoes the pattern in a different way. Even with the index near its highs at mid-summer, Goldman noted that the median S&P 500 stock sat more than 10% below its 52-week high, and market leadership remained narrow. Meanwhile, concentration is near record levels: the top 10 names hover around 38–40% of the index weight, highlighting how a few stocks can steady the surface while many move underneath.

Dispersion isn’t static. It spiked in April as tariff headlines hit, then eased back toward lows this summer. That cycle is the point: dispersion breathes. The task isn’t to predict the swings but to show steady proof of progress—evidence that survives both the chaos of a drawdown and the calm of a rally.

Signal vs. Noise

Price of Time — The 10-year term premium is positive again (around 0.7–0.8%), a reminder that investors get paid to wait. Long promises are worth less.

ESG Voting Reset — U.S. shareholders rejected all environmental proposals in the 2025 proxy season. E fizzled. G won.

Power Constraint — AI data center demand is straining the power grid. Interconnection requests can take up to seven years. And interest in nuclear/liquid cooling is on the rise.

One Last Thing

Markets are rewarding clarity over volume. Three realities are shaping this tape: power is scarce, time carries a price, and claims need operating proof. If you can demonstrate how work has changed, how the board is planning through policy noise, and how your metrics evolve from quarter to quarter, the story will carry.

If this letter resonated with you—or you want to keep this conversation going—I’d love to hear from you.

Until next month,

— Zachary